It’s easy to get tunnel vision when you’re building a new home and it’s nearing completion. You can practically feel that beautiful wooden banister and picture your shoe collection in that marvelous walk-in closet. These visions keep you going when your home is being built, but before you pack up those shoes, you want to make sure you understand the loan process, especially how your permanent loan finalizes.

Recent Posts

Prospective home buyers are finding more leverage through a 20% year-over-year increase in housing inventory, combined with cooling sticker prices for homes. A few of these buyers may be able to locate an assumable mortgage with a low rate from early 2021. While the housing "thaw" provides some relief, inflation is still affecting consumer spending, although showing signs of cooling slightly.

Are you having a rough time finding the exact home that meets your vision? Then building your dream home may be the right strategy for you. A custom home can take a few forms.

This label encompasses everything from buying a newly built home that allows for a few customized home plans to hiring a custom home builder who can tailor every plank, light switch, and master bedroom angle to your exact specifications.

Building your dream home is the most amazing thing ever (next to your kids), but like your kids, it requires careful planning and consideration. There are upfront tasks and considerations that may not come to mind, especially if you’ve purchased an existing home before and feel like this isn’t your first rodeo.

As a medical professional, you’ve dedicated countless hours to building your career and caring for others. Whether you’re a newly graduated doctor, dentist, or veterinarian, or an experienced professional, owning a home can feel like a distant goal. Student debt, limited credit history, and the high costs of buying a property add hurdles to achieving this milestone. Fortunately, the Doctor Loan program is here to change that.

Doctors, dentists, podiatrists, veterinarians, pharmacists, and CRNAs have some of the highest student loan balances and may have a difficult time qualifying for a mortgage when compared to other professionals. Lenders underwrite loan transactions using a calculation for student loan payments that can keep these highly trained professionals out of the housing market.

A “Doctor Loan” was designed to assist medical professionals in getting into a home with a low down payment while avoiding costly private mortgage insurance (PMI). They’ve been around for many years, but with the renewed focus on student loan debt, they’re making a bit of a comeback.

REACH YOUR GOALS

Five Reasons to File Your Taxes Sooner

There are two types of tax filers: those of us who file as soon as possible, and those who put it off until mid-April. If you're one of the millions who procrastinate, here are some reasons for filing early this year.

As the months ahead take shape, many people are looking for ways to improve their cash flow, exploring options that range from checking their eligibility for a health savings account (HSA) to buying and selling through the growing recommerce market. While mortgage interest rates have fallen, creating new opportunities for home purchases and refinancing, some buyers are still choosing to wait for property prices to cool.

Buying vs. renting real estate will always be a personal decision—one that should be based on your lifestyle, goals, and financial well-being. Factors like interest rates, the housing market, and what others around you are doing can be influential, but the ultimate decision is up to you.

Putting all that aside, here are some pros and cons of buying vs. renting that you should consider when determining whether buying vs. renting is better for you.

REACH YOUR GOALS

Start 2026 with the Right Budgeting App

While there's no shortage of budgeting applications available, current user rates suggest that many consumers find it difficult to choose the right one. Recent studies found that while around 45% of consumers use spreadsheets and calculators, only around 21% use budgeting applications.

As we step into a new year, it's a great time to reset, refocus, and look ahead with optimism. We hope the weeks ahead bring you and your loved ones good health, meaningful moments together, and plenty of reasons to feel hopeful about what's next.

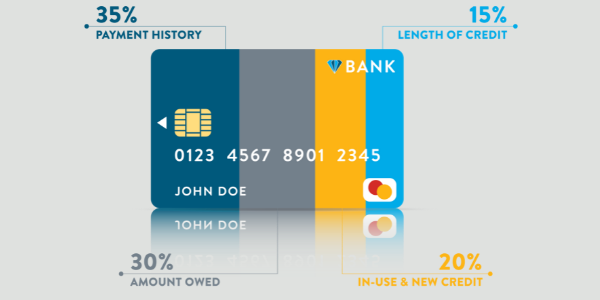

You know credit scores are important, but you may be wondering how they are calculated and what the big deal is. This all-important number can be looked at for a multitude of reasons: when you get a job, lease an apartment, open a new account, or apply for a loan---including a home loan.

Before you go shopping for a new home, you'll want to ensure that you meet the credit score requirements to secure a mortgage loan. And while many factors go into qualifying, a good credit score is definitely one of them.

We know that getting "rated" can make you feel like you're back in school. Like in school, however, with a bit of hard work, discipline, and dedication, you can improve your credit scores quickly!

So let's jump right in, starting with the obvious.

It's true that credit is an important part of qualifying for a home loan, but it's not the end-all and be-all. Buying a home with no credit is possible---the process just takes a few extra steps. Those steps can depend on a few factors, including whether you have a cosigner, as well as the size of your down payment. They will also depend on what type of home loan you're pursuing.

The holiday season is here, bringing friends and family together to celebrate. Here's wishing you a festive season and a prosperous New Year.

Rising costs continue to make news as we close out the year, with everything from insurance premiums to groceries putting pressure on household budgets. Some food costs have even spiked significantly compared to last year. The job market has shown mixed signals as well, with unemployment edging higher even as monthly job gains continue.

The holiday season is jam-packed with parties, shopping, cooking, gift-giving, and obligations. With all this going on, you might assume that the festive season is the worst time to buy or sell real estate.

Mortgage rates have been a roller-coaster ride this year, leaving many homeowners wondering whether now is the right time to buy a home, refinance their existing mortgage, or simply stay put.

A quick mortgage review can help you uncover ways to save money, access cash, or position yourself for future financial goals, especially if you bought or refinanced in the past few years. Whether rates move up or down next, knowing where you stand puts you in control.