Housing budgets are serious discussions because homes are serious investments. Home buyers expect to pay a down payment when buying a home. That amount can range based on qualification and the amount of assets available. Down payments start as low as 3% and can go as high as needed to get the payment at that comfort level.

But what some homebuyers accidentally overlook are the closing costs and fees associated with their mortgage loan.

Let’s start with closing costs. Closing costs typically represent 2% to 4% of the home’s purchase price and vary by state.

When you buy a home, you should expect to pay:

- Property taxes

- Transfer tax

- Title insurance

- Recording fees

- Appraisal fees

- Settlement or attorney’s fees

- Lender fees

- Discount points (if buying down the rate)

Additionally, you may have costs associated with a home inspection and appraisal, both performed by third parties. There is no application fee to apply for a mortgage.

These fees are calculated as estimated closing costs and are provided to you at the time you make the application. Initially, these numbers are estimates that may vary depending on when your loan is scheduled to close and other factors. At least three business days before your home loan is set to close, your mortgage lender will provide you with a final closing disclosure that outlines your exact costs.

Your closing costs shouldn’t cause sticker shock as long as your mortgage lender was diligent about explaining these fees when they provided you with the loan estimate during the loan application process.

Paying Points

While upfront costs may seem daunting, reducing your monthly mortgage payment is where you can really save some cash and eliminate stress. This may seem like dollars and cents when you’re talking about saving $50 to a few hundred dollars a month, but over the course of a 30-year loan, that’s big, big bucks.

This is where discount points come into play. Discount points are a cost associated with buying down your mortgage interest rate, either through a permanent or temporary rate buydown.

Why would you want to use mortgage points to only “buy down” the interest rate of your loan temporarily? We’re glad you asked. That’s coming up, but first, let’s get to the basics.

Permanent Mortgage Rate Buydown

A permanent mortgage rate buydown allows you to pay an additional fee (discount points) to lower your interest rate for the life of the loan. You can purchase as little as 0.125 of a point and as much as 4 mortgage points (the point limit is set by mortgage lenders).

Before you come to the conclusion that everyone should buy the maximum number of mortgage points no matter what, here are a few considerations:

- Cost: Each point is equal to 1% of your loan. As mentioned above, mortgage points are part of closing costs, so you’ll have to come up with these fees upfront or negotiate with the seller to cover those through your agreed-upon purchase contract.

- Breakeven point: Unsure how long you plan to stay in your home? Then buying permanent mortgage points may not be for you. These fees can be pricey depending on your loan amount and the number of points you pay, so you want to ensure that you’ll be in the home long enough to break even on the upfront costs. Every loan is different, but the breakeven point is generally between years six and seven of your home loan.

Discuss your plans with your mortgage lender, as they can show you the numbers in black and white so you are making the right decision for your specific scenario.

Temporary Mortgage Rate Buydown

While the permanent buydown applies to the life of your loan, a temporary buydown reduces the interest rate on your mortgage during the first two years. Some buyers appreciate this option because it makes for a smoother transition into homeownership, especially after shelling out all that dough for the down payment; closing costs; home furnishings; and any repairs, renovations, or improvements.

APM offers a 2-1 temporary buydown, which reduces the interest rate on your loan for the first two years. In the first year, the rate is reduced by 2 percentage points from the original note rate. In the second year, the original rate is reduced by 1 percentage point. After that, your rate reverts back to the note rate for the remainder of the loan term.

Seller-Paid Buydowns

As mentioned above, getting the seller on your home purchase to cover the cost of your buydown is a great way to go. Covering your temporary or permanent buydown can be attractive to sellers, as it typically costs less than a price reduction and actually helps buyers more in the long run, making their home more attractive.

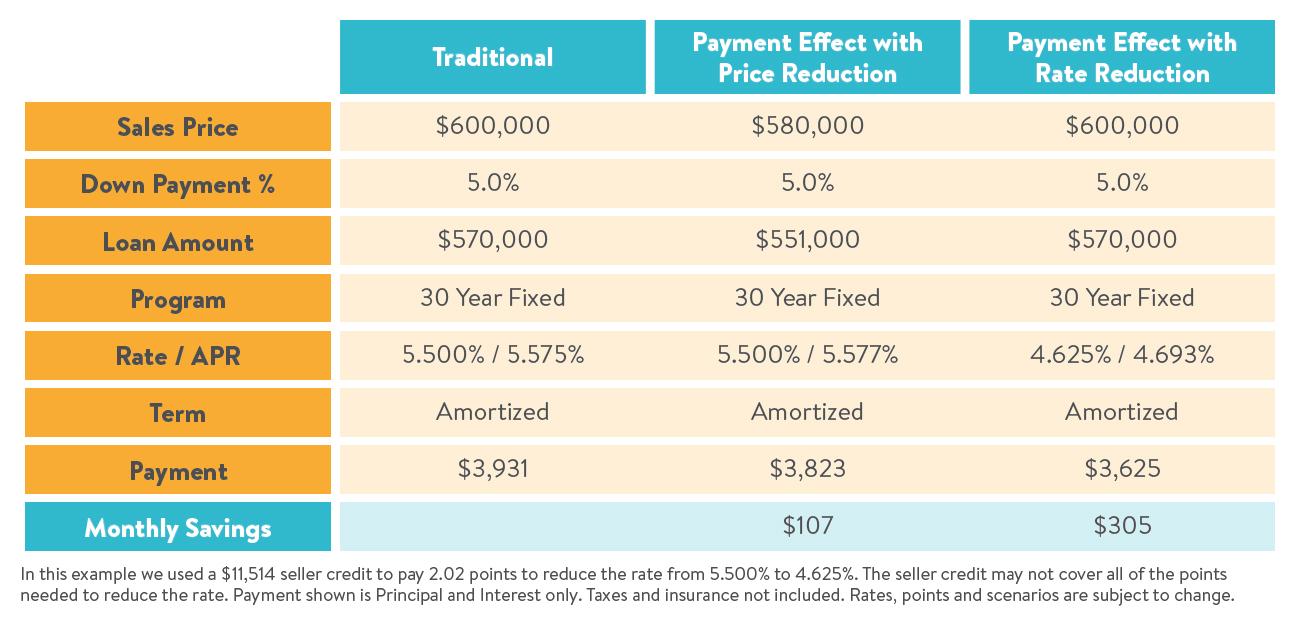

Sellers may be willing to cover the cost of a buydown if it means holding firm on their home’s purchase price. The buyer and the seller both have an advantage when this strategy is used over a price reduction. Let’s see an example:

In this example, we’re showing how much you would save if you asked the seller for a $20,000 price reduction (column 2) versus if you asked the seller to pay to buy down your interest rate (column 3).

Is Paying Points Right for You?

The money associated with closing costs typically won’t deter borrowers who plan to buy a home—and it shouldn’t. What can sometimes deter them, as we’re seeing now, is a rise in interest rates. Utilizing a permanent or temporary buydown can be a great way to offset these hikes and provide a little breathing room if you need it.

If you’ve gone over the financials and know how long you plan to stay in your home, mortgage points can be well worth the closing cost fees for some borrowers.

Ready for more information? Want to run a few different scenarios? Connect with an APM Loan Advisor in your area to review your options today.