By entering your information and clicking “submit," you agree that American Pacific Mortgage may call/text you about your inquiry, which may involve use of automated means and prerecorded/artificial voices. You do not need to consent as a condition of buying any property, goods or services. Message/data rates may apply.

Someone will be in contact with you shortly.

How is your credit?

Estimating your score will not harm your credit and will help us provide a range of available rates.

By entering your information and clicking “submit," you agree that American Pacific Mortgage may call/text you about your inquiry, which may involve use of automated means and prerecorded/artificial voices. You do not need to consent as a condition of buying any property, goods or services. Message/data rates may apply.

Someone will be in contact with you shortly.

By entering your information and clicking “submit," you agree that American Pacific Mortgage may call/text you about your inquiry, which may involve use of automated means and prerecorded/artificial voices. You do not need to consent as a condition of buying any property, goods or services. Message/data rates may apply.

Someone will be in contact with you shortly.

Applying with

is a breeze

To begin, you will need to create a secure account.

After you’ve created an account, you will enjoy:

- Secure loan application & document exchange

- Ability to pause and resume where you left off

- Updates on your application

- Capability to e-sign documents

- Easy access to resources

INFORMATION & RESOURCES

-

Opens modal dialog

Guide to VA Loans

Information about eligibility, costs, process, and more for buyers using their VA loan benefit -

Opens modal dialog

Understanding Credit

What drives a credit score, how to improve your credit, and easy ways to keep on track -

Opens modal dialog

Budgeting Workbook

Interactive worksheets to help you create a budget, financial goals, and debt payoff strategies to stay on track -

Free Download

Complete Guide to Realtor Business Planning

An interactive eBook with worksheets and goal setting materials to help you plan and grow your business

-

Opens modal dialog

Construction 101

Download our eBook to learn the ins and outs of preparing for and obtaining Construction Loans and much more! -

Opens modal dialog

Guide to Real Estate Investing

Anyone can own an investment property! Download our eBook to learn how to get started. -

Opens modal dialog

Unlocking Financial Freedom Through Debt Consolidation

Looking to consolidate your debt? Download our eBook to learn more.

Interactive Checklists

-

Download your free checklist

Credit Repair Checklist

An easy checklist to guide you in getting a copy of your credit report and fixing problems, as well as tips to improve your score -

Credit Repair Checklist (Spanish)

The Credit Repair Checklist translated for Spanish speakers -

Preparing for Home Ownership

A step-by-step checklist to keep you on track while preparing for your homeownership adventure -

Documents Requested

A list of the most common documents needed when applying for a home loan

-

Moving Checklist

A countdown checklist to keep track of all the details for your move to your new home -

Renovation Checklist

Our complimentary checklist will walk you through first steps, the documents and information you need to get your financing in place, and finishing up your project. -

Home Tour

Keep track of all the details during your home search

Infographics

-

A graphic available for download explaining the effect of interest rate on monthly mortgage payments

Effect of Interest Rate on Payment

A graphic explaining how payment is affected by interest rate -

An infographic available for download which provides an overview of the different ways to gather a down payment, comparing grants versus gifts versus down payment options

Grants vs Gifts vs Down Payment

An overview of the different ways to gather a down payment -

An infographic available for download which provides of overview of what drives the mortgage market and what makes rates rise and fall

What Drives Rates Infographic

An overview of what drives the mortgage market and what makes rates rise and fall -

A graphic available for download which highlights the effect of the loan amount on your monthly payment

Effect of Loan Amount on Payment

An examination of how the loan amount affects your loan payment

-

An easy-to-understand graphic for download which highlights things to know before you start saving for a down payment.

Strategies To Save

An easy-to-understand graphic with strategies to save a down payment -

Remodeling Returns

Add personal value to your home while improving its financial return

-

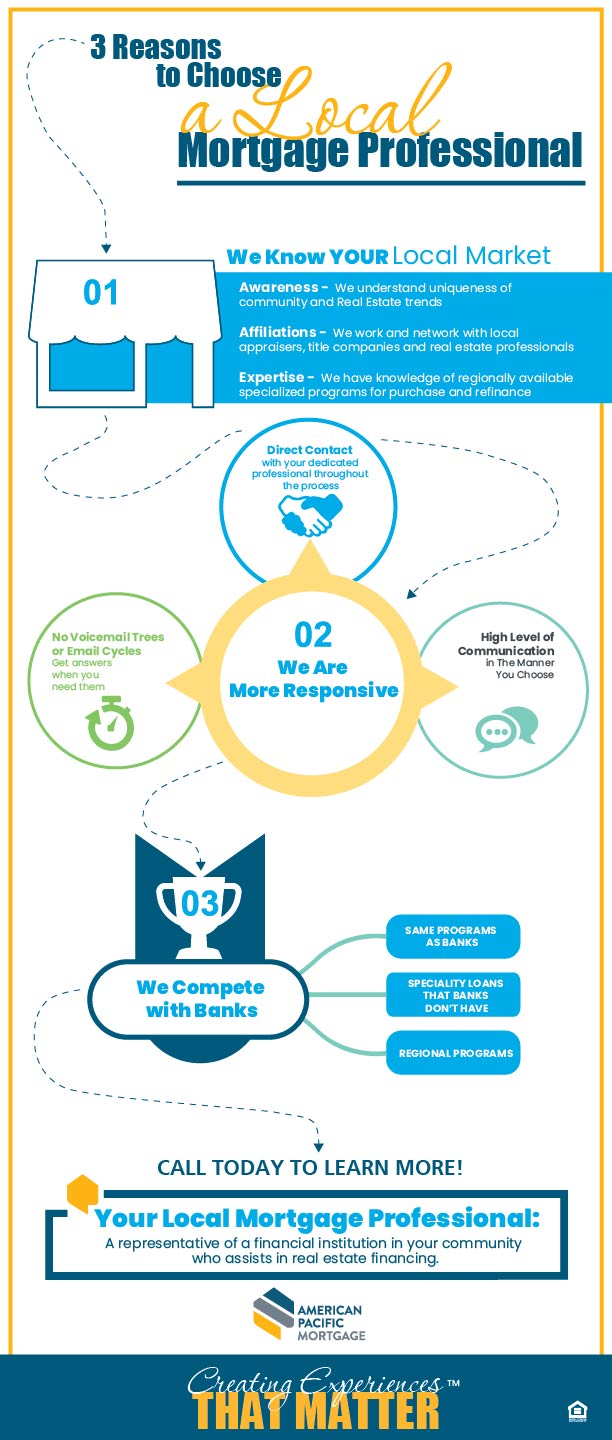

A graphic for download which shows the benefits of using a local mortgage professional

Benefits of Using Local Professional

Learn why using a professional who knows your market is so important -

Follow along with our steps to help successfully build your dream home

Steps to Building Your Dream Home

Follow along with our steps to help successfully build your dream home

-

Use our tips to help set up budgeting and finances for success

Tips for Budgeting to Buy a Home

Use our tips to help set up budgeting and finances for success -

Are you self-employed? Here's what you need to know for qualifying for a home loan

Qualifying for a home loan with self-employed income

Are you self-employed? Here's what you need to know for qualifying for a home loan -

Having issues with keeping your credit score high? Use these tips to improve your score

9 Tips to Improve Your Credit Score

Having issues with keeping your credit score high? Use these tips to improve your score -

The Pros and Cons of an Adjustable Rate Mortgage

Is an Adjustable-Rate Mortgage (ARM) Right for You?

The Pros and Cons of an Adjustable Rate Mortgage

We're Here to Help

We have even more articles, tidbits, and resources.

{kind=link}

{kind=link}